#sdsc6015

English / Chinese

Review - Convex Functions and Convex Optimization

Review

Review

A function f : R d → R f: \mathbb{R}^d \to \mathbb{R} f : R d → R

Its domain dom ( f ) \text{dom}(f) dom ( f )

For all x , y ∈ dom ( f ) \mathbf{x}, \mathbf{y} \in \text{dom}(f) x , y ∈ dom ( f ) λ ∈ [ 0 , 1 ] \lambda \in [0,1] λ ∈ [ 0 , 1 ]

f ( λ x + ( 1 − λ ) y ) ≤ λ f ( x ) + ( 1 − λ ) f ( y ) f(\lambda \mathbf{x} + (1-\lambda)\mathbf{y}) \leq \lambda f(\mathbf{x}) + (1-\lambda)f(\mathbf{y})

f ( λ x + ( 1 − λ ) y ) ≤ λ f ( x ) + ( 1 − λ ) f ( y )

Geometric Interpretation : The line segment between any two points on the function’s graph lies above the graph.

Review

If f f f

f ( y ) ≥ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) , ∀ x , y ∈ dom ( f ) f(\mathbf{y}) \geq f(\mathbf{x}) + \nabla f(\mathbf{x})^\top (\mathbf{y} - \mathbf{x}), \quad \forall \mathbf{x}, \mathbf{y} \in \text{dom}(f)

f ( y ) ≥ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) , ∀ x , y ∈ dom ( f )

Geometric Interpretation : The function graph always lies above its tangent hyperplane.

Review

Definition : f f f x 0 \mathbf{x}_0 x 0 ∇ f ( x 0 ) \nabla f(\mathbf{x}_0) ∇ f ( x 0 )

f ( x 0 + h ) ≈ f ( x 0 ) + ∇ f ( x 0 ) ⊤ h f(\mathbf{x}_0 + \mathbf{h}) \approx f(\mathbf{x}_0) + \nabla f(\mathbf{x}_0)^\top \mathbf{h}

f ( x 0 + h ) ≈ f ( x 0 ) + ∇ f ( x 0 ) ⊤ h

where h \mathbf{h} h

Globally Differentiable : If differentiable at every point in the domain, f f f

Review

Formulation:

min x ∈ R d f ( x ) \min_{\mathbf{x} \in \mathbb{R}^d} f(\mathbf{x})

x ∈ R d min f ( x )

where f f f R d \mathbb{R}^d R d x ∗ = arg min f ( x ) \mathbf{x}^* = \arg\min f(\mathbf{x}) x ∗ = arg min f ( x )

Gradient Descent Method

Core Idea

Update parameters using the negative gradient direction (gradient ∇ f ( x ) \nabla f(\mathbf{x}) ∇ f ( x )

x k + 1 = x k − η k ∇ f ( x k ) \mathbf{x}_{k+1} = \mathbf{x}_k - \eta_k \nabla f(\mathbf{x}_k)

x k + 1 = x k − η k ∇ f ( x k )

where:

x k \mathbf{x}_k x k k k k

η k \eta_k η k η k > 0 \eta_k > 0 η k > 0

∇ f ( x k ) \nabla f(\mathbf{x}_k) ∇ f ( x k ) f f f x k \mathbf{x}_k x k

x k + 1 \mathbf{x}_{k+1} x k + 1

Key Notes :

Gradient Direction : Negative gradient − ∇ f ( x k ) -\nabla f(\mathbf{x}_k) − ∇ f ( x k ) Step Size Selection :

Fixed step size (e.g., η k = 0.1 \eta_k = 0.1 η k = 0.1

Adaptive step size (e.g., η k = 1 k \eta_k = \frac{1}{\sqrt{k}} η k = k 1

Geometric Meaning : Each iteration moves linearly along the gradient direction by distance η k ∥ ∇ f ( x k ) ∥ \eta_k \|\nabla f(\mathbf{x}_k)\| η k ∥∇ f ( x k ) ∥

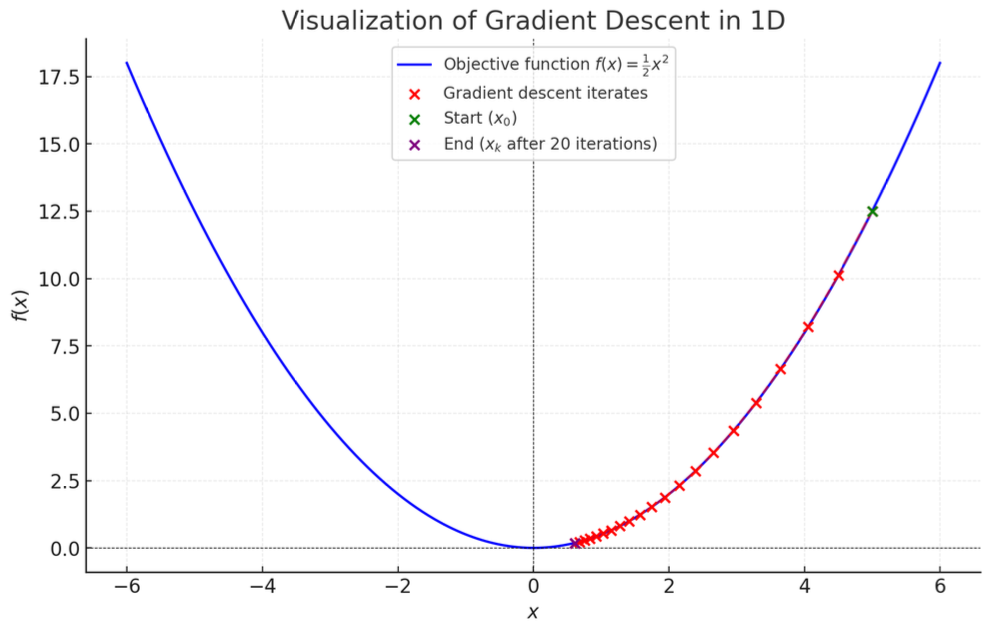

Gradient Descent Example: Quadratic Function Optimization

Consider the convex function f ( x ) = 1 2 x 2 f(x) = \frac{1}{2} x^2 f ( x ) = 2 1 x 2

Gradient Descent Update Rule

Iteration formula with fixed step size η \eta η

x t + 1 = x t − η ∇ f ( x t ) = x t − η x t = x t ( 1 − η ) x_{t+1} = x_t - \eta \nabla f(x_t) = x_t - \eta x_t = x_t (1 - \eta)

x t + 1 = x t − η ∇ f ( x t ) = x t − η x t = x t ( 1 − η )

After k k k

x k = x 0 ( 1 − η ) k x_k = x_0 (1 - \eta)^k

x k = x 0 ( 1 − η ) k

Derivation :

x k = x k − 1 ( 1 − η ) = x k − 2 ( 1 − η ) 2 = ⋯ = x 0 ( 1 − η ) k x_k = x_{k-1} (1 - \eta) = x_{k-2} (1 - \eta)^2 = \cdots = x_0 (1 - \eta)^k

x k = x k − 1 ( 1 − η ) = x k − 2 ( 1 − η ) 2 = ⋯ = x 0 ( 1 − η ) k

Convergence Analysis

When 0 < η < 1 0 < \eta < 1 0 < η < 1

lim k → ∞ x k = lim k → ∞ x 0 ( 1 − η ) k = 0 \lim_{k \to \infty} x_k = \lim_{k \to \infty} x_0 (1 - \eta)^k = 0

k → ∞ lim x k = k → ∞ lim x 0 ( 1 − η ) k = 0

Explanation :∣ 1 − η ∣ < 1 |1 - \eta| < 1 ∣1 − η ∣ < 1 ( 1 − η ) k (1 - \eta)^k ( 1 − η ) k x ∗ = 0 x^* = 0 x ∗ = 0

Convergence Behavior with Specific Parameters

Step Size : η = 0.1 \eta = 0.1 η = 0.1

Initial Point : x 0 = 5 x_0 = 5 x 0 = 5

Iteration Sequence :

x k = 5 × ( 0.9 ) k x_k = 5 \times (0.9)^k

x k = 5 × ( 0.9 ) k

Convergence Process :

k = 0 k=0 k = 0 x 0 = 5 x_0 = 5 x 0 = 5 k = 1 k=1 k = 1 x 1 = 5 × 0.9 = 4.5 x_1 = 5 \times 0.9 = 4.5 x 1 = 5 × 0.9 = 4.5 k = 10 k=10 k = 10 x 10 = 5 × ( 0.9 ) 10 ≈ 1.74 x_{10} = 5 \times (0.9)^{10} \approx 1.74 x 10 = 5 × ( 0.9 ) 10 ≈ 1.74 k = 50 k=50 k = 50 x 50 = 5 × ( 0.9 ) 50 ≈ 0.034 x_{50} = 5 \times (0.9)^{50} \approx 0.034 x 50 = 5 × ( 0.9 ) 50 ≈ 0.034

Conclusion :η = 0.1 \eta=0.1 η = 0.1 0 < η < 1 0<\eta<1 0 < η < 1 x ∗ = 0 x^*=0 x ∗ = 0

Vanilla Analysis of Gradient Descent

Goal: Bound the error f ( x t ) − f ( x ∗ ) f(\mathbf{x}_t) - f(\mathbf{x}^*) f ( x t ) − f ( x ∗ )

Define gradient g t : = ∇ f ( x t ) \mathbf{g}_t := \nabla f(\mathbf{x}_t) g t := ∇ f ( x t ) x t + 1 = x t − η g t \mathbf{x}_{t+1} = \mathbf{x}_t - \eta \mathbf{g}_t x t + 1 = x t − η g t

g t = x t − x t + 1 η \mathbf{g}_t = \frac{\mathbf{x}_t - \mathbf{x}_{t+1}}{\eta}

g t = η x t − x t + 1

Key Equality Derivation

Construct Inner Product Term :

g t ⊤ ( x t − x ∗ ) = 1 η ( x t − x t + 1 ) ⊤ ( x t − x ∗ ) \mathbf{g}_t^\top (\mathbf{x}_t - \mathbf{x}^*) = \frac{1}{\eta} (\mathbf{x}_t - \mathbf{x}_{t+1})^\top (\mathbf{x}_t - \mathbf{x}^*)

g t ⊤ ( x t − x ∗ ) = η 1 ( x t − x t + 1 ) ⊤ ( x t − x ∗ )

Apply Vector Identity (2 v ⊤ w = ∥ v ∥ 2 + ∥ w ∥ 2 − ∥ v − w ∥ 2 2\mathbf{v}^\top\mathbf{w} = \|\mathbf{v}\|^2 + \|\mathbf{w}\|^2 - \|\mathbf{v} - \mathbf{w}\|^2 2 v ⊤ w = ∥ v ∥ 2 + ∥ w ∥ 2 − ∥ v − w ∥ 2

g t ⊤ ( x t − x ∗ ) = 1 2 η ( ∥ x t − x t + 1 ∥ 2 + ∥ x t − x ∗ ∥ 2 − ∥ x t + 1 − x ∗ ∥ 2 ) = η 2 ∥ g t ∥ 2 + 1 2 η ( ∥ x t − x ∗ ∥ 2 − ∥ x t + 1 − x ∗ ∥ 2 ) \begin{aligned}

\mathbf{g}_t^\top (\mathbf{x}_t - \mathbf{x}^*)

&= \frac{1}{2\eta} \left( \|\mathbf{x}_t - \mathbf{x}_{t+1}\|^2 + \|\mathbf{x}_t - \mathbf{x}^*\|^2 - \|\mathbf{x}_{t+1} - \mathbf{x}^*\|^2 \right) \\

&= \frac{\eta}{2} \|\mathbf{g}_t\|^2 + \frac{1}{2\eta} \left( \|\mathbf{x}_t - \mathbf{x}^*\|^2 - \|\mathbf{x}_{t+1} - \mathbf{x}^*\|^2 \right)

\end{aligned}

g t ⊤ ( x t − x ∗ ) = 2 η 1 ( ∥ x t − x t + 1 ∥ 2 + ∥ x t − x ∗ ∥ 2 − ∥ x t + 1 − x ∗ ∥ 2 ) = 2 η ∥ g t ∥ 2 + 2 η 1 ( ∥ x t − x ∗ ∥ 2 − ∥ x t + 1 − x ∗ ∥ 2 )

Notes :

Term η 2 ∥ g t ∥ 2 \frac{\eta}{2} \|\mathbf{g}_t\|^2 2 η ∥ g t ∥ 2

Term 1 2 η ( ∥ x t − x ∗ ∥ 2 − ∥ x t + 1 − x ∗ ∥ 2 ) \frac{1}{2\eta} (\|\mathbf{x}_t - \mathbf{x}^*\|^2 - \|\mathbf{x}_{t+1} - \mathbf{x}^*\|^2) 2 η 1 ( ∥ x t − x ∗ ∥ 2 − ∥ x t + 1 − x ∗ ∥ 2 )

Sum over T T T :

∑ t = 0 T − 1 g t ⊤ ( x t − x ∗ ) = η 2 ∑ t = 0 T − 1 ∥ g t ∥ 2 + 1 2 η ( ∥ x 0 − x ∗ ∥ 2 − ∥ x T − x ∗ ∥ 2 ) \sum_{t=0}^{T-1} \mathbf{g}_t^\top (\mathbf{x}_t - \mathbf{x}^*) = \frac{\eta}{2} \sum_{t=0}^{T-1} \|\mathbf{g}_t\|^2 + \frac{1}{2\eta} \left( \|\mathbf{x}_0 - \mathbf{x}^*\|^2 - \|\mathbf{x}_T - \mathbf{x}^*\|^2 \right)

t = 0 ∑ T − 1 g t ⊤ ( x t − x ∗ ) = 2 η t = 0 ∑ T − 1 ∥ g t ∥ 2 + 2 η 1 ( ∥ x 0 − x ∗ ∥ 2 − ∥ x T − x ∗ ∥ 2 )

Combine with First-Order Convexity Condition

From convexity: f ( x ∗ ) ≥ f ( x t ) + g t ⊤ ( x ∗ − x t ) f(\mathbf{x}^*) \geq f(\mathbf{x}_t) + \mathbf{g}_t^\top (\mathbf{x}^* - \mathbf{x}_t) f ( x ∗ ) ≥ f ( x t ) + g t ⊤ ( x ∗ − x t )

f ( x t ) − f ( x ∗ ) ≤ g t ⊤ ( x t − x ∗ ) f(\mathbf{x}_t) - f(\mathbf{x}^*) \leq \mathbf{g}_t^\top (\mathbf{x}_t - \mathbf{x}^*)

f ( x t ) − f ( x ∗ ) ≤ g t ⊤ ( x t − x ∗ )

Substitute into summation for cumulative error bound:

∑ t = 0 T − 1 [ f ( x t ) − f ( x ∗ ) ] ≤ η 2 ∑ t = 0 T − 1 ∥ g t ∥ 2 + 1 2 η ( ∥ x 0 − x ∗ ∥ 2 − ∥ x T − x ∗ ∥ 2 ) \sum_{t=0}^{T-1} \left[ f(\mathbf{x}_t) - f(\mathbf{x}^*) \right] \leq \frac{\eta}{2} \sum_{t=0}^{T-1} \|\mathbf{g}_t\|^2 + \frac{1}{2\eta} \left( \|\mathbf{x}_0 - \mathbf{x}^*\|^2 - \|\mathbf{x}_T - \mathbf{x}^*\|^2 \right)

t = 0 ∑ T − 1 [ f ( x t ) − f ( x ∗ ) ] ≤ 2 η t = 0 ∑ T − 1 ∥ g t ∥ 2 + 2 η 1 ( ∥ x 0 − x ∗ ∥ 2 − ∥ x T − x ∗ ∥ 2 )

Key Conclusions :

Cumulative error is controlled by gradient norm sum ∑ ∥ g t ∥ 2 \sum \|\mathbf{g}_t\|^2 ∑ ∥ g t ∥ 2 ∥ x 0 − x ∗ ∥ 2 \|\mathbf{x}_0 - \mathbf{x}^*\|^2 ∥ x 0 − x ∗ ∥ 2

Step Size η \eta η :

Too large: Gradient term η 2 ∑ ∥ g t ∥ 2 \frac{\eta}{2} \sum \|\mathbf{g}_t\|^2 2 η ∑ ∥ g t ∥ 2

Too small: Distance term 1 2 η ∥ x 0 − x ∗ ∥ 2 \frac{1}{2\eta} \|\mathbf{x}_0 - \mathbf{x}^*\|^2 2 η 1 ∥ x 0 − x ∗ ∥ 2

Convergence Analysis for Lipschitz Convex Functions

Assume all gradients of f have bounded norm.

Equivalent to f f f

Excludes many interesting functions (e.g., f ( x ) = x 2 f(x) = x^2 f ( x ) = x 2

Equivalence Proof

Let f : R d → R f: \mathbb{R}^d \to \mathbb{R} f : R d → R

Bounded Gradient : ∃ M > 0 \exists M > 0 ∃ M > 0 ∥ ∇ f ( x ) ∥ ≤ M , ∀ x \|\nabla f(x)\| \leq M, \ \forall x ∥∇ f ( x ) ∥ ≤ M , ∀ x

Lipschitz Continuity : ∃ L > 0 \exists L > 0 ∃ L > 0 ∥ f ( y ) − f ( x ) ∥ ≤ L ∥ y − x ∥ , ∀ x , y \|f(y) - f(x)\| \leq L \|y - x\|, \ \forall x, y ∥ f ( y ) − f ( x ) ∥ ≤ L ∥ y − x ∥ , ∀ x , y

Proof Outline (⇒) Bounded Gradient ⇒ Lipschitz Continuity Assume ∥ ∇ f ( x ) ∥ ≤ M \|\nabla f(x)\| \leq M ∥∇ f ( x ) ∥ ≤ M

f ( y ) − f ( x ) = ∫ 0 1 ∇ f ( x + t ( y − x ) ) ⊤ ( y − x ) d t f(y) - f(x) = \int_0^1 \nabla f(x + t(y-x))^\top (y-x) \, dt

f ( y ) − f ( x ) = ∫ 0 1 ∇ f ( x + t ( y − x ) ) ⊤ ( y − x ) d t

Take norms and apply Cauchy-Schwarz:

∥ f ( y ) − f ( x ) ∥ ≤ ∫ 0 1 ∥ ∇ f ( x + t ( y − x ) ) ∥ ⋅ ∥ y − x ∥ d t \|f(y) - f(x)\| \leq \int_0^1 \|\nabla f(x + t(y-x))\| \cdot \|y - x\| \, dt

∥ f ( y ) − f ( x ) ∥ ≤ ∫ 0 1 ∥∇ f ( x + t ( y − x )) ∥ ⋅ ∥ y − x ∥ d t

Substitute bounded gradient condition:

∥ f ( y ) − f ( x ) ∥ ≤ ∫ 0 1 M ∥ y − x ∥ d t = M ∥ y − x ∥ \|f(y) - f(x)\| \leq \int_0^1 M \|y - x\| \, dt = M \|y - x\|

∥ f ( y ) − f ( x ) ∥ ≤ ∫ 0 1 M ∥ y − x ∥ d t = M ∥ y − x ∥

Thus f f f M M M

Explanation : Bounded gradient norm controls function value change rate.

(⇐) Lipschitz Continuity ⇒ Bounded Gradient Assume ∥ f ( y ) − f ( x ) ∥ ≤ L ∥ y − x ∥ \|f(y) - f(x)\| \leq L \|y - x\| ∥ f ( y ) − f ( x ) ∥ ≤ L ∥ y − x ∥ f f f ∥ ∇ f ( x ) ∥ ≤ L \|\nabla f(x)\| \leq L ∥∇ f ( x ) ∥ ≤ L

If ∇ f ( x ) = 0 \nabla f(x) = 0 ∇ f ( x ) = 0 : Trivial.

Otherwise : Set y = x + ∇ f ( x ) y = x + \nabla f(x) y = x + ∇ f ( x )

f ( y ) ≥ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) f(y) \geq f(x) + \nabla f(x)^\top (y - x)

f ( y ) ≥ f ( x ) + ∇ f ( x ) ⊤ ( y − x )

Substitute y − x = ∇ f ( x ) y - x = \nabla f(x) y − x = ∇ f ( x )

f ( y ) − f ( x ) ≥ ∇ f ( x ) ⊤ ∇ f ( x ) = ∥ ∇ f ( x ) ∥ 2 ( ∗ ) f(y) - f(x) \geq \nabla f(x)^\top \nabla f(x) = \|\nabla f(x)\|^2 \quad (*)

f ( y ) − f ( x ) ≥ ∇ f ( x ) ⊤ ∇ f ( x ) = ∥∇ f ( x ) ∥ 2 ( ∗ )

By Lipschitz continuity:

f ( y ) − f ( x ) ≤ L ∥ y − x ∥ = L ∥ ∇ f ( x ) ∥ ( ∗ ∗ ) f(y) - f(x) \leq L \|y - x\| = L \|\nabla f(x)\| \quad (**)

f ( y ) − f ( x ) ≤ L ∥ y − x ∥ = L ∥∇ f ( x ) ∥ ( ∗ ∗ )

Combine ( ∗ ) (*) ( ∗ ) ( ∗ ∗ ) (**) ( ∗ ∗ )

∥ ∇ f ( x ) ∥ 2 ≤ L ∥ ∇ f ( x ) ∥ \|\nabla f(x)\|^2 \leq L \|\nabla f(x)\|

∥∇ f ( x ) ∥ 2 ≤ L ∥∇ f ( x ) ∥

Thus ∥ ∇ f ( x ) ∥ ≤ L \|\nabla f(x)\| \leq L ∥∇ f ( x ) ∥ ≤ L

Explanation : Lipschitz continuity restricts linear growth of function values, forcing bounded gradient norm.

Fundamental Theorem Application :

f ( y ) − f ( x ) = ∫ 0 1 ∇ f ( x + t ( y − x ) ) ⊤ ( y − x ) d t f(y) - f(x) = \int_0^1 \nabla f(x + t(y-x))^\top (y-x) \, dt

f ( y ) − f ( x ) = ∫ 0 1 ∇ f ( x + t ( y − x ) ) ⊤ ( y − x ) d t

Meaning : Expresses function difference as path integral of gradient.

Cauchy-Schwarz Inequality :

∣ ∇ f ( z ) ⊤ ( y − x ) ∣ ≤ ∥ ∇ f ( z ) ∥ ⋅ ∥ y − x ∥ \left| \nabla f(z)^\top (y-x) \right| \leq \|\nabla f(z)\| \cdot \|y - x\|

∇ f ( z ) ⊤ ( y − x ) ≤ ∥∇ f ( z ) ∥ ⋅ ∥ y − x ∥

Role : Converts inner product to norm product for integral bounding.

First-Order Convexity Condition :

f ( y ) ≥ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) f(y) \geq f(x) + \nabla f(x)^\top (y - x)

f ( y ) ≥ f ( x ) + ∇ f ( x ) ⊤ ( y − x )

Role : Establishes one-way relationship between gradient and function value change.

Appendix: P47 Example f ( x ) = ∣ x ∣ f(x) = |x| f ( x ) = ∣ x ∣

At x > 0 x > 0 x > 0 g k = 1 g_k = 1 g k = 1 x ∗ = 0 x^* = 0 x ∗ = 0

At x = 0 x = 0 x = 0 g k ∈ [ − 1 , 1 ] g_k \in [-1, 1] g k ∈ [ − 1 , 1 ]

Theorem Setup Let f : R d → R f: \mathbb{R}^d \to \mathbb{R} f : R d → R

∥ x 0 − x ∗ ∥ ≤ R \|\mathbf{x}_0 - \mathbf{x}^*\| \leq R ∥ x 0 − x ∗ ∥ ≤ R

∥ ∇ f ( x ) ∥ ≤ B , ∀ x \|\nabla f(\mathbf{x})\| \leq B,\ \forall \mathbf{x} ∥∇ f ( x ) ∥ ≤ B , ∀ x B B B f f f

Convergence Proof

Base Inequality (from Vanilla Analysis):

∑ t = 0 T − 1 [ f ( x t ) − f ( x ∗ ) ] ≤ η 2 ∑ t = 0 T − 1 ∥ g t ∥ 2 + 1 2 η ∥ x 0 − x ∗ ∥ 2 \sum_{t=0}^{T-1} [f(\mathbf{x}_t) - f(\mathbf{x}^*)] \leq \frac{\eta}{2} \sum_{t=0}^{T-1} \|\mathbf{g}_t\|^2 + \frac{1}{2\eta} \|\mathbf{x}_0 - \mathbf{x}^*\|^2

t = 0 ∑ T − 1 [ f ( x t ) − f ( x ∗ )] ≤ 2 η t = 0 ∑ T − 1 ∥ g t ∥ 2 + 2 η 1 ∥ x 0 − x ∗ ∥ 2

Substitute Bounded Conditions :

∑ t = 0 T − 1 [ f ( x t ) − f ( x ∗ ) ] ≤ η 2 B 2 T + R 2 2 η \sum_{t=0}^{T-1} [f(\mathbf{x}_t) - f(\mathbf{x}^*)] \leq \frac{\eta}{2} B^2 T + \frac{R^2}{2\eta}

t = 0 ∑ T − 1 [ f ( x t ) − f ( x ∗ )] ≤ 2 η B 2 T + 2 η R 2

Optimize Step Size η \eta η :

h ( η ) = η B 2 T 2 + R 2 2 η h(\eta) = \frac{\eta B^2 T}{2} + \frac{R^2}{2\eta}

h ( η ) = 2 η B 2 T + 2 η R 2

Optimal step size via derivative:h ′ ( η ) = B 2 T 2 − R 2 2 η 2 = 0 ⇒ η ∗ = R B T h'(\eta) = \frac{B^2 T}{2} - \frac{R^2}{2\eta^2} = 0 \ \Rightarrow \ \eta^* = \frac{R}{B\sqrt{T}}

h ′ ( η ) = 2 B 2 T − 2 η 2 R 2 = 0 ⇒ η ∗ = B T R

Substitute for minimal bound:h ( η ∗ ) = R B T ⋅ B 2 T 2 + R 2 2 ⋅ R B T = R B T h(\eta^*) = \frac{R}{B\sqrt{T}} \cdot \frac{B^2 T}{2} + \frac{R^2}{2 \cdot \frac{R}{B\sqrt{T}}} = RB\sqrt{T}

h ( η ∗ ) = B T R ⋅ 2 B 2 T + 2 ⋅ B T R R 2 = RB T

Average Error Bound

1 T ∑ t = 0 T − 1 [ f ( x t ) − f ( x ∗ ) ] ≤ R B T \frac{1}{T} \sum_{t=0}^{T-1} [f(\mathbf{x}_t) - f(\mathbf{x}^*)] \leq \frac{RB}{\sqrt{T}}

T 1 t = 0 ∑ T − 1 [ f ( x t ) − f ( x ∗ )] ≤ T RB

Convergence Rate and Iteration Count

Note : Lipschitz condition excludes functions with unbounded gradients (e.g., f ( x ) = x 2 f(x)=x^2 f ( x ) = x 2

Practical Advice (Unknown R R R B B B

Fixed Small Step Size : Start with η = 0.01 \eta = 0.01 η = 0.01

Dynamic Adjustment :

Oscillation/divergence → decrease η \eta η

Or use decaying step size η t = η 0 t + 1 \eta_t = \frac{\eta_0}{\sqrt{t+1}} η t = t + 1 η 0

Adaptive Methods : Use adaptive optimizers like Adam

Smooth Functions

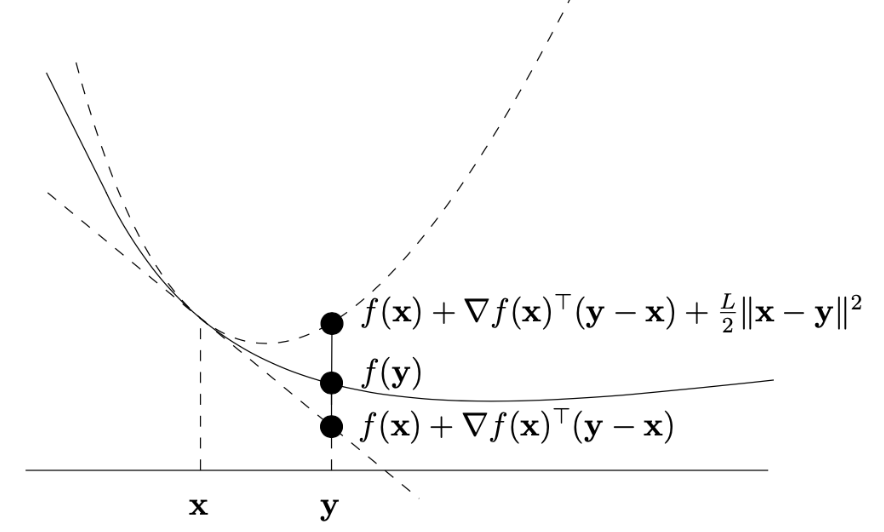

Definition

A differentiable function f : dom ( f ) → R f : \text{dom}(f) \to \mathbb{R} f : dom ( f ) → R smooth with parameter L > 0 L > 0 L > 0 X ⊆ dom ( f ) X \subseteq \text{dom}(f) X ⊆ dom ( f ) x , y ∈ X x, y \in X x , y ∈ X

f ( y ) ≤ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) + L 2 ∥ x − y ∥ 2 f(y) \leq f(x) + \nabla f(x)^\top (y - x) + \frac{L}{2} \|x - y\|^2

f ( y ) ≤ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) + 2 L ∥ x − y ∥ 2

Intuition :

The function “does not bend too much,” its growth is bounded by a quadratic function (like a paraboloid).

L L L L L L

Geometric Interpretation

Smoothness implies: Near any point x x x f f f

Example :f ( x ) = x 2 f(x) = x^2 f ( x ) = x 2

Operations Preserving Smoothness

The following operations preserve smoothness under specified conditions:

Lemma 1 f 1 , … , f m f_1, \dots, f_m f 1 , … , f m L 1 , … , L m L_1, \dots, L_m L 1 , … , L m λ 1 , … , λ m ∈ R + \lambda_1, \dots, \lambda_m \in \mathbb{R}^+ λ 1 , … , λ m ∈ R + f : = ∑ i = 1 m λ i f i f := \sum_{i=1}^m \lambda_i f_i f := ∑ i = 1 m λ i f i ∑ i = 1 m λ i L i \sum_{i=1}^m \lambda_i L_i ∑ i = 1 m λ i L i f f f L L L g : R m → R d g: \mathbb{R}^m \to \mathbb{R}^d g : R m → R d g ( x ) = A x + b g(x) = Ax + b g ( x ) = A x + b A ∈ R d × m A \in \mathbb{R}^{d \times m} A ∈ R d × m b ∈ R d b \in \mathbb{R}^d b ∈ R d f ∘ g f \circ g f ∘ g x ↦ f ( A x + b ) x \mapsto f(Ax + b) x ↦ f ( A x + b ) L ∥ A ∥ 2 L \|A\|_2 L ∥ A ∥ 2

Here ∥ A ∥ 2 \|A\|_2 ∥ A ∥ 2 spectral norm of A A A

Convex vs. Smooth Functions: Properties and Optimization

Basic Concept Comparison

Property

Mathematical Definition

Geometric Meaning

Optimization Implication

Convexity f ( λ x + ( 1 − λ ) y ) ≤ λ f ( x ) + ( 1 − λ ) f ( y ) f(\lambda x + (1-\lambda)y) \leq \lambda f(x) + (1-\lambda)f(y) f ( λ x + ( 1 − λ ) y ) ≤ λ f ( x ) + ( 1 − λ ) f ( y ) Graph below chords

Guarantees global optimality

Lipschitz Continuity ∣ ∇ f ( x ) ∣ ≤ B |\nabla f(x)| \leq B ∣∇ f ( x ) ∣ ≤ B Bounded gradient, controlled change rate

Controls gradient descent stability

Smoothness ∣ ∇ f ( x ) − ∇ f ( y ) ∣ ≤ L ∣ x − y ∣ |\nabla f(x) - \nabla f(y)| \leq L|x-y| ∣∇ f ( x ) − ∇ f ( y ) ∣ ≤ L ∣ x − y ∣ Gentle gradient changes, bounded curvature

Enables faster convergence rates

Key Equivalence

Lemma 2: Equivalent Characterizations of Smoothness

For convex differentiable f : R d → R f: \mathbb{R}^d \to \mathbb{R} f : R d → R

f f f L L L f ( y ) ≤ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) + L 2 ∥ x − y ∥ 2 f(y) \leq f(x) + \nabla f(x)^\top(y-x) + \frac{L}{2}\|x-y\|^2 f ( y ) ≤ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) + 2 L ∥ x − y ∥ 2

Gradient is L L L ∥ ∇ f ( x ) − ∇ f ( y ) ∥ ≤ L ∥ x − y ∥ \|\nabla f(x) - \nabla f(y)\| \leq L\|x-y\| ∥∇ f ( x ) − ∇ f ( y ) ∥ ≤ L ∥ x − y ∥

Significance : Establishes equivalence between function smoothness and gradient Lipschitz continuity.

Gradient Descent Analysis for Smooth Functions

Lemma 3: Sufficient Decrease

For L L L η = 1 L \eta = \frac{1}{L} η = L 1

f ( x t + 1 ) ≤ f ( x t ) − 1 2 L ∥ ∇ f ( x t ) ∥ 2 f(x_{t+1}) \leq f(x_t) - \frac{1}{2L} \|\nabla f(x_t)\|^2

f ( x t + 1 ) ≤ f ( x t ) − 2 L 1 ∥∇ f ( x t ) ∥ 2

Proof :

f ( x t + 1 ) ≤ f ( x t ) + ∇ f ( x t ) ⊤ ( x t + 1 − x t ) + L 2 ∥ x t + 1 − x t ∥ 2 = f ( x t ) − 1 L ∥ ∇ f ( x t ) ∥ 2 + 1 2 L ∥ ∇ f ( x t ) ∥ 2 = f ( x t ) − 1 2 L ∥ ∇ f ( x t ) ∥ 2 \begin{aligned}

f(x_{t+1}) &\leq f(x_t) + \nabla f(x_t)^\top(x_{t+1}-x_t) + \frac{L}{2}\|x_{t+1}-x_t\|^2 \\

&= f(x_t) - \frac{1}{L} \|\nabla f(x_t)\|^2 + \frac{1}{2L} \|\nabla f(x_t)\|^2 \\

&= f(x_t) - \frac{1}{2L} \|\nabla f(x_t)\|^2

\end{aligned}

f ( x t + 1 ) ≤ f ( x t ) + ∇ f ( x t ) ⊤ ( x t + 1 − x t ) + 2 L ∥ x t + 1 − x t ∥ 2 = f ( x t ) − L 1 ∥∇ f ( x t ) ∥ 2 + 2 L 1 ∥∇ f ( x t ) ∥ 2 = f ( x t ) − 2 L 1 ∥∇ f ( x t ) ∥ 2

Meaning : Each iteration guarantees function value decrease, controlled by gradient norm.

Theorem 2: Convergence Rate

For L L L f f f η = 1 L \eta = \frac{1}{L} η = L 1

f ( x T ) − f ( x ∗ ) ≤ L ∥ x 0 − x ∗ ∥ 2 2 T f(x_T) - f(x^*) \leq \frac{L \|x_0 - x^*\|^2}{2T}

f ( x T ) − f ( x ∗ ) ≤ 2 T L ∥ x 0 − x ∗ ∥ 2

Proof Sketch :

Use base analysis inequality

Apply sufficient decrease lemma to bound gradient term

Obtain final bound via telescoping sum

Practical Applications and Comparisons

Convergence Rate Comparison

Function Type

Convergence Rate

Iteration Complexity (ε \varepsilon ε

Lipschitz Convex

O ( 1 / T ) O(1/\sqrt{T}) O ( 1/ T ) O ( 1 / ε 2 ) O(1/\varepsilon^2) O ( 1/ ε 2 )

Smooth Convex

O ( 1 / T ) O(1/T) O ( 1/ T ) O ( 1 / ε ) O(1/\varepsilon) O ( 1/ ε )

Advantage : Smoothness improves convergence from sublinear to linear, significantly boosting efficiency.

Practical Advice: Unknown L L L

Initial Guess : Set L = 2 ε R 2 L = \frac{2\varepsilon}{R^2} L = R 2 2 ε

Verification : Check f ( x t + 1 ) ≤ f ( x t ) − 1 2 L ∥ ∇ f ( x t ) ∥ 2 f(x_{t+1}) \leq f(x_t) - \frac{1}{2L} \|\nabla f(x_t)\|^2 f ( x t + 1 ) ≤ f ( x t ) − 2 L 1 ∥∇ f ( x t ) ∥ 2

Doubling Strategy : If condition fails, double L L L

Total Complexity : At most O ( 4 R 2 L ε ) O\left(\frac{4R^2L}{\varepsilon}\right) O ( ε 4 R 2 L ) ε \varepsilon ε

Practical Impact : Adaptive adjustment enables efficient optimization even without knowing L L L

Subgradient Method

Subgradient Definition

For convex f : R d → R f: \mathbb{R}^d \to \mathbb{R} f : R d → R x \mathbf{x} x g ∈ R d \mathbf{g} \in \mathbb{R}^d g ∈ R d

f ( y ) ≥ f ( x ) + g ⊤ ( y − x ) , ∀ y f(\mathbf{y}) \geq f(\mathbf{x}) + \mathbf{g}^\top (\mathbf{y} - \mathbf{x}), \quad \forall \mathbf{y}

f ( y ) ≥ f ( x ) + g ⊤ ( y − x ) , ∀ y

Key Properties :

Always exists at points in the domain

If f f f x \mathbf{x} x ∇ f ( x ) \nabla f(\mathbf{x}) ∇ f ( x )

Subgradient Calculation Examples

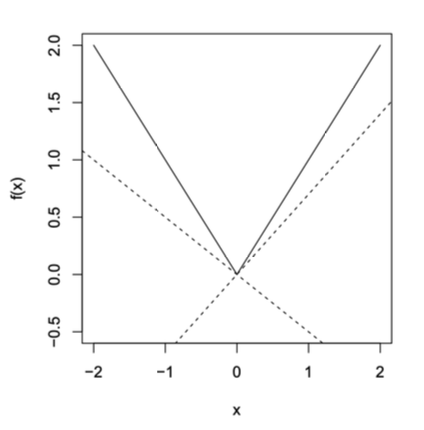

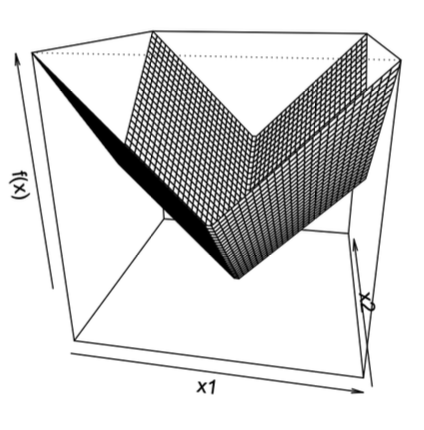

Example 1: Absolute Value f ( x ) = ∣ x ∣ f(x) = |x| f ( x ) = ∣ x ∣

For x ≠ 0 x \neq 0 x = 0 g = sign ( x ) g = \text{sign}(x) g = sign ( x )

For x = 0 x = 0 x = 0 g ∈ [ − 1 , 1 ] g \in [-1, 1] g ∈ [ − 1 , 1 ]

Example 2: L2 Norm f ( x ) = ∥ x ∥ 2 f(\mathbf{x}) = \|\mathbf{x}\|_2 f ( x ) = ∥ x ∥ 2

For x ≠ 0 \mathbf{x} \neq \mathbf{0} x = 0 g = x ∥ x ∥ 2 \mathbf{g} = \frac{\mathbf{x}}{\|\mathbf{x}\|_2} g = ∥ x ∥ 2 x

For x = 0 \mathbf{x} = \mathbf{0} x = 0 g \mathbf{g} g { z : ∥ z ∥ 2 ≤ 1 } \{\mathbf{z} : \|\mathbf{z}\|_2 \leq 1\} { z : ∥ z ∥ 2 ≤ 1 }

Example 3: L1 Norm f ( x ) = ∥ x ∥ 1 = ∑ i = 1 d ∣ x i ∣ f(\mathbf{x}) = \|\mathbf{x}\|_1 = \sum_{i=1}^d |x_i| f ( x ) = ∥ x ∥ 1 = ∑ i = 1 d ∣ x i ∣

For x i ≠ 0 x_i \neq 0 x i = 0 g i = sign ( x i ) g_i = \text{sign}(x_i) g i = sign ( x i )

For x i = 0 x_i = 0 x i = 0 g i ∈ [ − 1 , 1 ] g_i \in [-1, 1] g i ∈ [ − 1 , 1 ]

Example 4: Set Indicator Function

For convex set X ⊂ R d X \subset \mathbb{R}^d X ⊂ R d

1 X ( x ) = { 0 if x ∈ X + ∞ if x ∉ X 1_X(\mathbf{x}) =

\begin{cases}

0 & \text{if } \mathbf{x} \in X \\

+\infty & \text{if } \mathbf{x} \notin X

\end{cases}

1 X ( x ) = { 0 + ∞ if x ∈ X if x ∈ / X

Normal Cone

Definition : For convex set X ⊆ R d X \subseteq \mathbb{R}^d X ⊆ R d x ∈ X \mathbf{x} \in X x ∈ X

N X ( x ) = { g ∈ R d ∣ g ⊤ x ≥ g ⊤ y , ∀ y ∈ X } \mathcal{N}_X(\mathbf{x}) = \{ \mathbf{g} \in \mathbb{R}^d \mid \mathbf{g}^\top \mathbf{x} \geq \mathbf{g}^\top \mathbf{y},\ \forall \mathbf{y} \in X \}

N X ( x ) = { g ∈ R d ∣ g ⊤ x ≥ g ⊤ y , ∀ y ∈ X }

Geometric Interpretation : Contains outward-pointing vectors “supporting” X X X x \mathbf{x} x x \mathbf{x} x

Subdifferential

Definition : The subdifferential of convex f : R d → R f: \mathbb{R}^d \to \mathbb{R} f : R d → R x \mathbf{x} x

∂ f ( x ) = { g ∈ R d ∣ f ( y ) ≥ f ( x ) + g ⊤ ( y − x ) , ∀ y ∈ R d } \partial f(\mathbf{x}) = \{ \mathbf{g} \in \mathbb{R}^d \mid f(\mathbf{y}) \geq f(\mathbf{x}) + \mathbf{g}^\top (\mathbf{y} - \mathbf{x}),\ \forall \mathbf{y} \in \mathbb{R}^d \}

∂ f ( x ) = { g ∈ R d ∣ f ( y ) ≥ f ( x ) + g ⊤ ( y − x ) , ∀ y ∈ R d }

Properties :

∂ f ( x ) \partial f(\mathbf{x}) ∂ f ( x )

If f f f x \mathbf{x} x ∂ f ( x ) = { ∇ f ( x ) } \partial f(\mathbf{x}) = \{ \nabla f(\mathbf{x}) \} ∂ f ( x ) = { ∇ f ( x )}

If ∂ f ( x ) \partial f(\mathbf{x}) ∂ f ( x ) f f f x \mathbf{x} x ∇ f ( x ) = g \nabla f(\mathbf{x}) = \mathbf{g} ∇ f ( x ) = g

Optimality Conditions

Unconstrained Optimization

For convex f : R d → R f: \mathbb{R}^d \to \mathbb{R} f : R d → R

x ∗ minimizes f ⟺ 0 ∈ ∂ f ( x ∗ ) \mathbf{x}^* \text{ minimizes } f \iff 0 \in \partial f(\mathbf{x}^*)

x ∗ minimizes f ⟺ 0 ∈ ∂ f ( x ∗ )

Interpretation : x ∗ \mathbf{x}^* x ∗

Constrained Optimization

Consider:

min x f ( x ) s.t. x ∈ X \min_{\mathbf{x}} f(\mathbf{x}) \quad \text{s.t.} \quad \mathbf{x} \in X

x min f ( x ) s.t. x ∈ X

Reformulation : Introduce indicator function 1 X ( x ) 1_X(\mathbf{x}) 1 X ( x )

min x { f ( x ) + 1 X ( x ) } \min_{\mathbf{x}} \left\{ f(\mathbf{x}) + 1_X(\mathbf{x}) \right\}

x min { f ( x ) + 1 X ( x ) }

Optimality Condition : x ∗ ∈ X \mathbf{x}^* \in X x ∗ ∈ X

0 ∈ ∂ ( f ( x ∗ ) + 1 X ( x ∗ ) ) = ∇ f ( x ∗ ) + N X ( x ∗ ) 0 \in \partial \left( f(\mathbf{x}^*) + 1_X(\mathbf{x}^*) \right) = \nabla f(\mathbf{x}^*) + \mathcal{N}_X(\mathbf{x}^*)

0 ∈ ∂ ( f ( x ∗ ) + 1 X ( x ∗ ) ) = ∇ f ( x ∗ ) + N X ( x ∗ )

Equivalently:

− ∇ f ( x ∗ ) ∈ N X ( x ∗ ) - \nabla f(\mathbf{x}^*) \in \mathcal{N}_X(\mathbf{x}^*)

− ∇ f ( x ∗ ) ∈ N X ( x ∗ )

By normal cone definition, this means:

∇ f ( x ∗ ) ⊤ ( y − x ∗ ) ≥ 0 , ∀ y ∈ X \nabla f(\mathbf{x}^*)^\top (\mathbf{y} - \mathbf{x}^*) \geq 0, \quad \forall \mathbf{y} \in X

∇ f ( x ∗ ) ⊤ ( y − x ∗ ) ≥ 0 , ∀ y ∈ X

Geometric Interpretation : At optimum x ∗ \mathbf{x}^* x ∗

Subgradient Method

Basic Concepts

For a convex function f : R d → R f : \mathbb{R}^d \to \mathbb{R} f : R d → R subgradient instead of the gradient:

x k + 1 = x k − η k + 1 g k x_{k+1} = x_k - \eta_{k+1} g_k

x k + 1 = x k − η k + 1 g k

x k x_k x k

g k ∈ ∇ f ( x k ) g_k \in \nabla f(x_k) g k ∈ ∇ f ( x k ) f f f x k x_k x k

η k > 0 \eta_k > 0 η k > 0

x k + 1 x_{k+1} x k + 1

⚠️ Note: The subgradient method is not necessarily a descent method. For example, when f ( x ) = ∣ x ∣ f(x) = |x| f ( x ) = ∣ x ∣

Convergence Theorem

Theorem 3 : Assume f f f L-Lipschitz (i.e., ∣ f ( x ) − f ( y ) ∣ ≤ L ∥ x − y ∥ |f(x) - f(y)| \leq L \|x - y\| ∣ f ( x ) − f ( y ) ∣ ≤ L ∥ x − y ∥

Fixed step size η k = η \eta_k = \eta η k = η k k k

lim k → ∞ f ( x best ( k ) ) ≤ f ∗ + L 2 η 2 \lim_{k \to \infty} f(x_{\text{best}}^{(k)}) \leq f^* + \frac{L^2 \eta}{2}

k → ∞ lim f ( x best ( k ) ) ≤ f ∗ + 2 L 2 η

Diminishing step size (satisfying ∑ k = 1 ∞ η k 2 < ∞ \sum_{k=1}^\infty \eta_k^2 < \infty ∑ k = 1 ∞ η k 2 < ∞ ∑ k = 1 ∞ η k = ∞ \sum_{k=1}^\infty \eta_k = \infty ∑ k = 1 ∞ η k = ∞

lim k → ∞ f ( x best ( k ) ) ≤ f ∗ \lim_{k \to \infty} f(x_{\text{best}}^{(k)}) \leq f^*

k → ∞ lim f ( x best ( k ) ) ≤ f ∗

Where:

f ( x best ( k ) ) = min i = 0 , … , k f ( x i ) f(x_{\text{best}}^{(k)}) = \min_{i=0,\dots,k} f(x_i) f ( x best ( k ) ) = min i = 0 , … , k f ( x i ) k k k f ∗ = f ( x ∗ ) f^* = f(x^*) f ∗ = f ( x ∗ )

Key Steps of the Proof

Based on the definition of the subgradient, we can derive the basic inequality:

∥ x k − x ∗ ∥ 2 ≤ ∥ x k − 1 − x ∗ ∥ 2 − 2 η k ( f ( x k − 1 ) − f ∗ ) + η k 2 ∥ g k − 1 ∥ 2 \|x_k - x^*\|^2 \leq \|x_{k-1} - x^*\|^2 - 2\eta_k (f(x_{k-1}) - f^*) + \eta_k^2 \|g_{k-1}\|^2

∥ x k − x ∗ ∥ 2 ≤ ∥ x k − 1 − x ∗ ∥ 2 − 2 η k ( f ( x k − 1 ) − f ∗ ) + η k 2 ∥ g k − 1 ∥ 2

Iterating this inequality and rearranging (let R = ∥ x 0 − x ∗ ∥ R = \|x_0 - x^*\| R = ∥ x 0 − x ∗ ∥

0 ≤ R 2 − 2 ∑ i = 1 k η i ( f ( x i − 1 ) − f ∗ ) + L 2 ∑ i = 1 k η i 2 0 \leq R^2 - 2 \sum_{i=1}^k \eta_i (f(x_{i-1}) - f^*) + L^2 \sum_{i=1}^k \eta_i^2

0 ≤ R 2 − 2 i = 1 ∑ k η i ( f ( x i − 1 ) − f ∗ ) + L 2 i = 1 ∑ k η i 2

After introducing f ( x best ( k ) ) f(x_{\text{best}}^{(k)}) f ( x best ( k ) ) basic inequality :

f ( x best ( k ) ) − f ∗ ≤ R 2 + L 2 ∑ i = 1 k η i 2 2 ∑ i = 1 k η i f(x_{\text{best}}^{(k)}) - f^* \leq \frac{R^2 + L^2 \sum_{i=1}^k \eta_i^2}{2 \sum_{i=1}^k \eta_i}

f ( x best ( k ) ) − f ∗ ≤ 2 ∑ i = 1 k η i R 2 + L 2 ∑ i = 1 k η i 2

The convergence results for different step size strategies can be derived from this.

Convergence Rate with Fixed Step Size

If the step size is fixed as η \eta η

f ( x best ( k ) ) − f ∗ ≤ R 2 2 k η + L 2 η 2 f(x_{\text{best}}^{(k)}) - f^* \leq \frac{R^2}{2k\eta} + \frac{L^2 \eta}{2}

f ( x best ( k ) ) − f ∗ ≤ 2 k η R 2 + 2 L 2 η

To achieve accuracy f ( x best ( k ) ) − f ∗ ≤ ε f(x_{\text{best}}^{(k)}) - f^* \leq \varepsilon f ( x best ( k ) ) − f ∗ ≤ ε ≤ ε / 2 \leq \varepsilon/2 ≤ ε /2

Therefore, the convergence rate of the subgradient method is O ( 1 ε 2 ) O\left(\frac{1}{\varepsilon^2}\right) O ( ε 2 1 )

📉 Comparison: The convergence rate of gradient descent for smooth convex functions is O ( 1 ε ) O\left(\frac{1}{\varepsilon}\right) O ( ε 1 )

Summary of Algorithm Convergence

Function Properties

Algorithm

Convergence Bound

Number of Iterations

Convex, L-Lipschitz

Subgradient

f ( x best ( T ) ) − f ∗ ≤ L R T f(x_{\text{best}}^{(T)}) - f^* \leq \frac{LR}{\sqrt{T}} f ( x best ( T ) ) − f ∗ ≤ T L R O ( R 2 L 2 ε 2 ) O\left(\frac{R^2 L^2}{\varepsilon^2}\right) O ( ε 2 R 2 L 2 )

Convex, L-Smooth

Gradient Descent

f ( x best ( T ) ) − f ∗ ≤ R 2 L 2 T f(x_{\text{best}}^{(T)}) - f^* \leq \frac{R^2 L}{2T} f ( x best ( T ) ) − f ∗ ≤ 2 T R 2 L O ( R 2 L ε ) O\left(\frac{R^2 L}{\varepsilon}\right) O ( ε R 2 L )

Convex, L-Lipschitz

Gradient Descent

f ( x best ( T ) ) − f ∗ ≤ R L T f(x_{\text{best}}^{(T)}) - f^* \leq \frac{RL}{\sqrt{T}} f ( x best ( T ) ) − f ∗ ≤ T R L O ( R 2 L 2 ε 2 ) O\left(\frac{R^2 L^2}{\varepsilon^2}\right) O ( ε 2 R 2 L 2 )

Where:

T T T R = ∥ x 0 − x ∗ ∥ R = \|x_0 - x^*\| R = ∥ x 0 − x ∗ ∥ x best ( T ) = arg min i = 0 , 1 , … , T f ( x i ) x_{\text{best}}^{(T)} = \arg\min_{i=0,1,\dots,T} f(x_i) x best ( T ) = arg min i = 0 , 1 , … , T f ( x i ) T T T

Summary

Expand

Convex Function Definition

f : R d → R f: \mathbb{R}^d \to \mathbb{R} f : R d → R

dom ( f ) \text{dom}(f) dom ( f )

∀ x , y ∈ dom ( f ) , λ ∈ [ 0 , 1 ] \forall \mathbf{x}, \mathbf{y} \in \text{dom}(f), \lambda \in [0,1] ∀ x , y ∈ dom ( f ) , λ ∈ [ 0 , 1 ]

f ( λ x + ( 1 − λ ) y ) ≤ λ f ( x ) + ( 1 − λ ) f ( y ) f(\lambda \mathbf{x} + (1-\lambda)\mathbf{y}) \leq \lambda f(\mathbf{x}) + (1-\lambda)f(\mathbf{y})

f ( λ x + ( 1 − λ ) y ) ≤ λ f ( x ) + ( 1 − λ ) f ( y )

Geometry : Line segment between graph points lies above graph.

First-Order Convexity

If f f f

f ( y ) ≥ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) f(\mathbf{y}) \geq f(\mathbf{x}) + \nabla f(\mathbf{x})^\top (\mathbf{y} - \mathbf{x})

f ( y ) ≥ f ( x ) + ∇ f ( x ) ⊤ ( y − x )

Geometry : Graph above tangent hyperplane.

Differentiable Functions

Definition : f f f x 0 \mathbf{x}_0 x 0 ∃ ∇ f ( x 0 ) \exists \nabla f(\mathbf{x}_0) ∃∇ f ( x 0 )

f ( x 0 + h ) ≈ f ( x 0 ) + ∇ f ( x 0 ) ⊤ h f(\mathbf{x}_0 + \mathbf{h}) \approx f(\mathbf{x}_0) + \nabla f(\mathbf{x}_0)^\top \mathbf{h}

f ( x 0 + h ) ≈ f ( x 0 ) + ∇ f ( x 0 ) ⊤ h

Global Differentiability : Differentiable everywhere → non-vertical tangents everywhere.

Convex Optimization

Formulation:

min x ∈ R d f ( x ) \min_{\mathbf{x} \in \mathbb{R}^d} f(\mathbf{x})

x ∈ R d min f ( x )

f f f R d \mathbb{R}^d R d x ∗ = arg min f ( x ) \mathbf{x}^* = \arg\min f(\mathbf{x}) x ∗ = arg min f ( x )

Gradient Descent

Core Idea

Update with negative gradient:

x k + 1 = x k − η k ∇ f ( x k ) \mathbf{x}_{k+1} = \mathbf{x}_k - \eta_k \nabla f(\mathbf{x}_k)

x k + 1 = x k − η k ∇ f ( x k )

Convergence Analysis

Lipschitz Convex Functions (Bounded Gradient)

Assumptions : ∥ ∇ f ( x ) ∥ ≤ B \|\nabla f(\mathbf{x})\| \leq B ∥∇ f ( x ) ∥ ≤ B ∥ x 0 − x ∗ ∥ ≤ R \|\mathbf{x}_0 - \mathbf{x}^*\| \leq R ∥ x 0 − x ∗ ∥ ≤ R Step Size : η = R B T \eta = \frac{R}{B\sqrt{T}} η = B T R Convergence Rate :

1 T ∑ t = 0 T − 1 [ f ( x t ) − f ( x ∗ ) ] ≤ R B T \frac{1}{T} \sum_{t=0}^{T-1} [f(\mathbf{x}_t) - f(\mathbf{x}^*)] \leq \frac{RB}{\sqrt{T}}

T 1 t = 0 ∑ T − 1 [ f ( x t ) − f ( x ∗ )] ≤ T RB

Advantage : Dimension-independent.Practice : Unknown B , R B, R B , R η \eta η

Smooth Convex Functions (Lipschitz Gradient)

Definition : f f f L L L

f ( y ) ≤ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) + L 2 ∥ x − y ∥ 2 f(\mathbf{y}) \leq f(\mathbf{x}) + \nabla f(\mathbf{x})^\top (\mathbf{y}-\mathbf{x}) + \frac{L}{2} \|\mathbf{x}-\mathbf{y}\|^2

f ( y ) ≤ f ( x ) + ∇ f ( x ) ⊤ ( y − x ) + 2 L ∥ x − y ∥ 2

≡ ∥ ∇ f ( x ) − ∇ f ( y ) ∥ ≤ L ∥ x − y ∥ \|\nabla f(\mathbf{x}) - \nabla f(\mathbf{y})\| \leq L \|\mathbf{x}-\mathbf{y}\| ∥∇ f ( x ) − ∇ f ( y ) ∥ ≤ L ∥ x − y ∥ Step Size : η = 1 L \eta = \frac{1}{L} η = L 1 Convergence Rate :

f ( x T ) − f ( x ∗ ) ≤ L ∥ x 0 − x ∗ ∥ 2 2 T f(\mathbf{x}_T) - f(\mathbf{x}^*) \leq \frac{L \|\mathbf{x}_0 - \mathbf{x}^*\|^2}{2T}

f ( x T ) − f ( x ∗ ) ≤ 2 T L ∥ x 0 − x ∗ ∥ 2

Comparison : O ( 1 / ε ) O(1/\varepsilon) O ( 1/ ε ) O ( 1 / ε 2 ) O(1/\varepsilon^2) O ( 1/ ε 2 ) Practice : Unknown L L L f ( x t + 1 ) ≤ f ( x t ) − 1 2 L ∥ ∇ f ( x t ) ∥ 2 f(\mathbf{x}_{t+1}) \leq f(\mathbf{x}_t) - \frac{1}{2L} \|\nabla f(\mathbf{x}_t)\|^2 f ( x t + 1 ) ≤ f ( x t ) − 2 L 1 ∥∇ f ( x t ) ∥ 2

Subgradient Method

Subgradient Definition

For convex f f f g ∈ ∂ f ( x ) g \in \partial f(\mathbf{x}) g ∈ ∂ f ( x )

f ( y ) ≥ f ( x ) + g ⊤ ( y − x ) , ∀ y f(\mathbf{y}) \geq f(\mathbf{x}) + g^\top (\mathbf{y} - \mathbf{x}), \quad \forall \mathbf{y}

f ( y ) ≥ f ( x ) + g ⊤ ( y − x ) , ∀ y

Key Properties :

∂ f ( x ) = { ∇ f ( x ) } \partial f(\mathbf{x}) = \{\nabla f(\mathbf{x})\} ∂ f ( x ) = { ∇ f ( x )} Optimality: x ∗ \mathbf{x}^* x ∗ 0 ∈ ∂ f ( x ∗ ) 0 \in \partial f(\mathbf{x}^*) 0 ∈ ∂ f ( x ∗ )

Update Rule

x k + 1 = x k − η k g k , g k ∈ ∂ f ( x k ) \mathbf{x}_{k+1} = \mathbf{x}_k - \eta_k g_k, \quad g_k \in \partial f(\mathbf{x}_k)

x k + 1 = x k − η k g k , g k ∈ ∂ f ( x k )

Note : Not a descent method (e.g., oscillates for f ( x ) = ∣ x ∣ f(x)=|x| f ( x ) = ∣ x ∣

Convergence

Assumptions : f f f L L L

Fixed η \eta η : Limiting error ≤ f ∗ + L 2 η / 2 \leq f^* + L^2\eta/2 ≤ f ∗ + L 2 η /2

Diminishing η \eta η (∑ η k = ∞ \sum \eta_k = \infty ∑ η k = ∞ ∑ η k 2 < ∞ \sum \eta_k^2 < \infty ∑ η k 2 < ∞ f ∗ f^* f ∗ Convergence Rate :

f ( x best ( k ) ) − f ∗ ≤ R 2 + L 2 ∑ i = 1 k η i 2 2 ∑ i = 1 k η i f(\mathbf{x}_{\text{best}}^{(k)}) - f^* \leq \frac{R^2 + L^2 \sum_{i=1}^k \eta_i^2}{2 \sum_{i=1}^k \eta_i}

f ( x best ( k ) ) − f ∗ ≤ 2 ∑ i = 1 k η i R 2 + L 2 ∑ i = 1 k η i 2

where R = ∥ x 0 − x ∗ ∥ R = \|\mathbf{x}_0 - \mathbf{x}^*\| R = ∥ x 0 − x ∗ ∥ f best ( k ) = min i = 0 , … , k f ( x i ) f_{\text{best}}^{(k)} = \min_{i=0,\dots,k} f(\mathbf{x}_i) f best ( k ) = min i = 0 , … , k f ( x i )